If you’ve started researching the homebuying process, you’ve probably heard both terms — “pre-qualification” and “pre-approval” — used almost interchangeably. They’re not the same thing, and confusing the two can cost you your dream home.

Don’t worry — you’re not alone. This is one of the most common points of confusion for homebuyers, and by the end of this article, you’ll know exactly what each one means, which one you need, and when you need it.

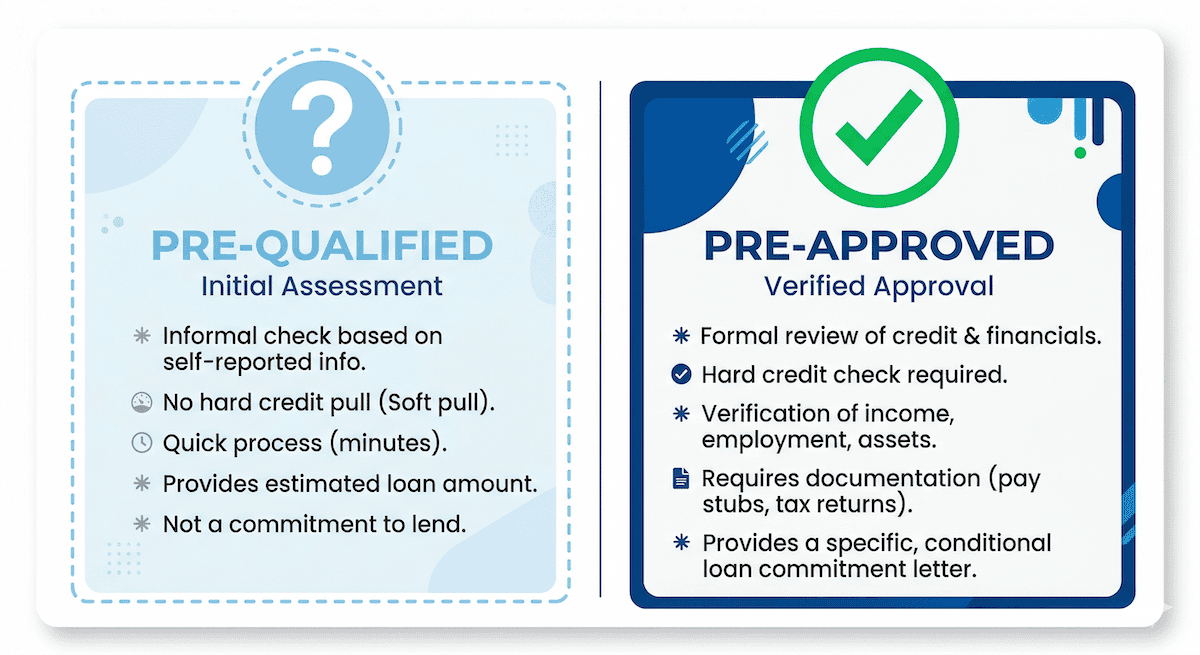

What Is Mortgage Pre-Qualification?

Think of pre-qualification as a quick financial snapshot. It’s typically a short conversation (or online form) with a lender where you share basic information about your income, assets, debts, and employment — mostly self-reported, with no formal verification required.

Based on that information, the lender gives you an estimate of how much you might be able to borrow. It’s fast, it’s usually free, and it typically doesn’t require a hard credit pull.

Pre-qualification is great for:

- Getting a general idea of your budget early in your home search

- Understanding what price ranges make sense before you start touring homes

- Figuring out what financial areas you may need to improve before applying

What pre-qualification is NOT:

- A guarantee of financing

- Something a seller will take seriously in a competitive market

- A substitute for a full pre-approval

What Is Mortgage Pre-Approval?

Pre-approval is the real deal. This is a formal, lender-verified commitment that says you qualify to borrow up to a specific loan amount. To issue a pre-approval, a lender will:

- Pull your credit report (this is a hard inquiry)

- Verify your income with W-2s, tax returns, and/or pay stubs

- Review your bank statements and assets

- Verify your employment history

- Calculate your debt-to-income ratio (DTI)

After reviewing all of this, the lender issues a pre-approval letter — a written document stating the loan amount you’re approved for, the loan type, and an expiration date (typically 60–90 days).

Pre-approval is what you need when:

- You’re ready to seriously shop for a home

- You want sellers to take your offer seriously

- You’re competing with other buyers (which is common in the Scottsdale and Phoenix markets)

Why the Difference Matters So Much

Here’s where it gets real: In a competitive market like Scottsdale or Phoenix, submitting an offer with only a pre-qualification letter can get your offer thrown in the trash.

Listing agents advise their sellers to look for the strongest, most credible offers. A pre-approval letter signals to the seller that a lender has already done their homework on you — you’re a verified, serious buyer. A pre-qualification letter just says you think you can afford it.

Imagine two offers come in on the same home at the same price. One buyer has a pre-qualification. The other has a full pre-approval. Which offer do you think the seller accepts? The pre-approved buyer wins nearly every time.

In fast-moving markets, some sellers and their agents won’t even schedule a showing without a pre-approval letter in hand.

What About “Verified Approval” or “Underwritten Pre-Approval”?

Some lenders take it one step further with what’s often called a verified approval or underwritten pre-approval. This means an actual underwriter — not just a loan officer — has reviewed your file and conditionally approved your loan before you’ve even found a home.

This is the gold standard. In highly competitive situations (like multiple-offer scenarios on Scottsdale luxury homes), an underwritten pre-approval can make your offer nearly as strong as a cash offer in the seller’s eyes.

If your lender offers this option, it’s worth asking about it early in the process.

Common Questions Buyers Ask

Does getting pre-approved hurt my credit score?

Yes, a hard credit inquiry will cause a small, temporary dip — typically 5 points or less. But here’s the good news: if you apply with multiple lenders within a short window (usually 14–45 days), the credit bureaus treat it as a single inquiry for rate-shopping purposes. So don’t be afraid to shop around.

When should I get pre-approved?

Before you start touring homes seriously. You don’t want to fall in love with a home and then spend a week scrambling to get your paperwork together while another buyer snatches it up.

How long does pre-approval last?

Most pre-approval letters are valid for 60–90 days. If your home search goes longer than that, you’ll simply update your documents and get a refreshed letter.

Can my pre-approval be taken away?

Yes — and this is important. Your pre-approval is based on your financial picture at the time of application. If you open a new credit card, finance a car, quit your job, or make a large unexplained cash deposit during your home search, it can jeopardize your loan. Keep your finances stable from the moment you get pre-approved until after closing.

A Simple Way to Remember the Difference

Here’s an easy analogy:

Pre-qualification is like telling a restaurant you think you’ll come to dinner.

Pre-approval is a confirmed reservation.

Sellers want confirmed reservations.

Your Next Step

If you’re thinking about buying a home in the Scottsdale or Phoenix area — whether it’s your first home or your fifth — the smartest first step is to connect with a trusted local lender and get fully pre-approved before you fall in love with a listing.

Once you have your pre-approval letter in hand, you’ll have a clear budget, real credibility with sellers, and the confidence to move fast when the right home comes along.